Please note that this is not intended to be a full summary of the CARES Act. Instead, I have reviewed those portions of the CARES Act that I thought would be most important to our clients and our network. However, I have intentionally omitted discussions on the amount of relief that will be paid to individuals and families, as others have adequately covered and summarized such topics. See for example here, where you can calculate what you (as an individual taxpayer) will receive (if anything).

I have focused my discussion on the SBA 7(a) Loans. There are two types of SBA Loans that you may be hearing about. First is the economic injury disaster loan (EIDL) and the second is the Section 7(a) Loans. Both have different application processes. There were only certain parts of EIDL that was amended as part of the CARES Act. The main changes were made to the 7(a) Loans.

EIDL loan terms have some differences from 7(a) loans (including a lower interest rate (2.75% to 3.75%, a longer term (up to 30 years)). For more information on EIDL loans (or to apply) go here.

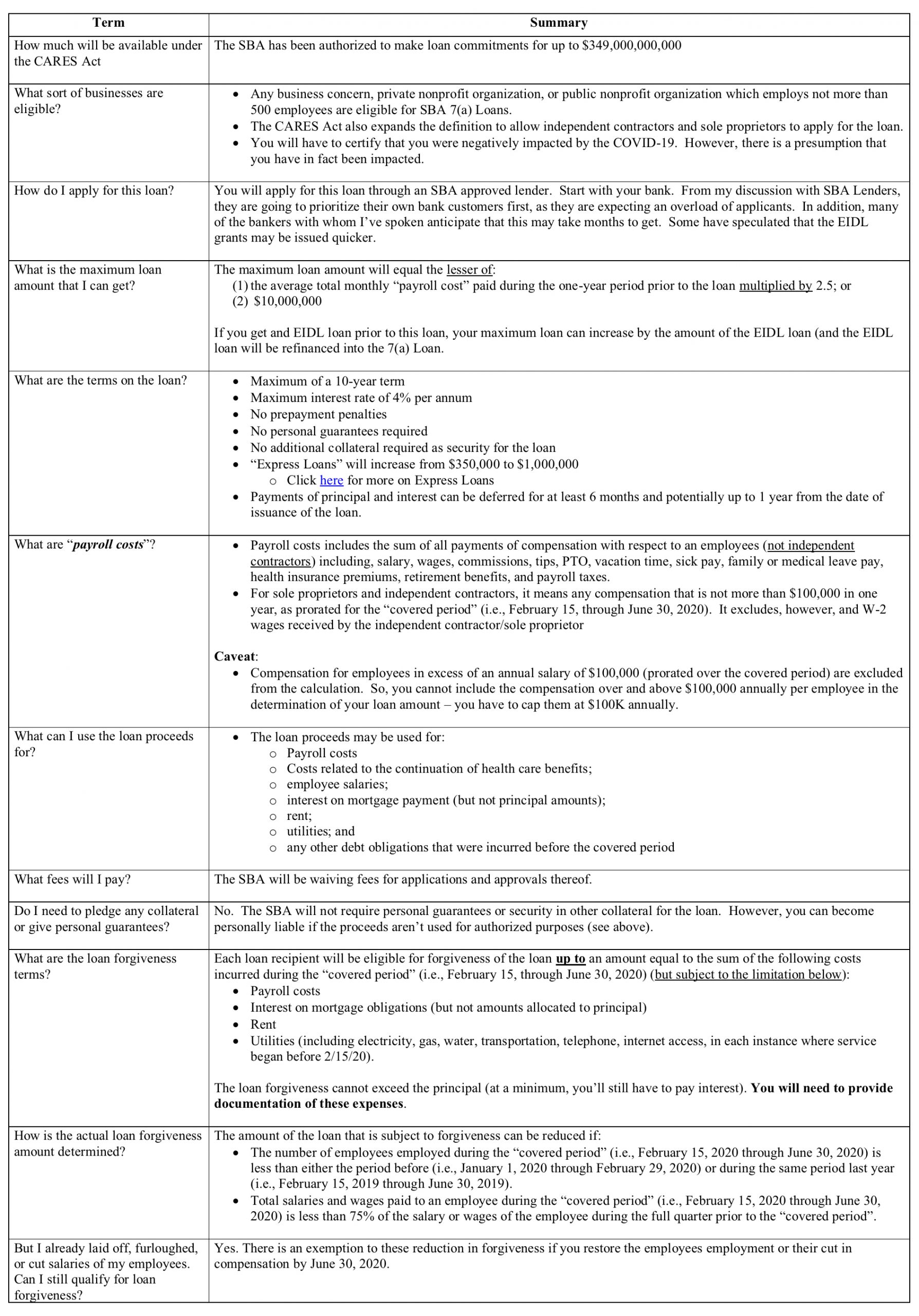

Below is a summary of the major terms and answers to the questions that you may have about the SBA 7(a) Loans under the CARES Act. There are certainly more nuances; but, I have tried to distill these concepts in plain English for you to get a basic understanding.

SBA 7(A) LOAN PROGRAM

ADDITIONAL INFORMATION

If you’re considering a 7(a) Loan, we recommend that you start with an SBA lender at your current bank. If you’d like a referral to a trusted SBA Lender, please let us know and we can help you get connected.

Stay Up-To-Date

To stay on top of alerts like this and other timely business matters, be sure to sign up for our free monthly newsletter and bookmark our COVID-19 Business Resource page.